Sinking ship: Barack Obama's approval rating now at Bush levels-37%

Options

Comments

-

kingblaze84 wrote: »FuriousOne wrote: »!kingblaze84 wrote: »FuriousOne wrote: »kingblaze84 wrote: »

Obamacare is not a good alternative because IT IS TOO ? EXPENSIVE FOR THE AVG AMERICAN WITHOUT HEALTH INSURANCE. Single payer is not favored by Republicans true, but many independents and Democrats do support it. I'm sure it's a very popular idea among Americans based on polls I've seen. That is what should have been fought for, even in a losing effort (in this environment politically). To tell Americans they MUST sign up for expensive as hell exchanges is ridiculous and not something people are going to be enthusiastic about.

Let's talk about my homegirl for a minute who has two kids. The cheapest plan she saw was $312 a month to cover her and her fam on the website. She makes ten bucks an hour LOL how the ? can she afford that in NY? Really anywhere? The Unaffordable Care Act will still leave a shitload of people uninsured cuz many can't afford this. The law has to be changed like crazy or destroyed the way slavery and prohibition was destroyed. Cuz at this rate, young and healthy people aren't gonna ? with this, including myself. I have retirement to save for, and I'll gladly wait for single payer to arrive or at least until more affordable health insurance comes along, something I'm close to finding thanks to some research I'm doing in NY (amgmedicalgroup.com)......those without health insurance aren't ? with the website for a reason homie, aside from the neverending glitches on the site.

From that very website ? .

FAMILY PLANS FOR $446.00 PER MONTH

Do they cover rare disease or broken legs? What's the cap for the year if the expenses are too much? What if the procedure is 20 thou? Good luck when you trip down some stairs at 45. Medicare will not cover that and I'm sure you will not be retired yet at that point. Not wishing that on you, just saying, life is that random. Your friend has two kids and I'm sure she's not getting any good ass apartments in NY at $10 an hour pre obamacare either but with those kids, i imagine she actually is covered for a lot more then you claiming. What's her rent like btw? Section 8? Anybody bring in money in her household? This picture isn't clear enough at all.

I'm sure they'll fix the website but you're not signing up so what do you care? Being that you in NYC though, how are you having issues with the website when after you put in your zip, it takes you to a NYC based website? I'm sure things would have worked better if red states provided their own portals.

You and Obama don't get it. This is penalizing people for not being able to afford healthcare, how is this the consumers fault for the most part when the govt printing dollars like Monopoly money is the reason why people can't afford this via inflation? Costs are only gona get higher as young people ? on this law by deciding to pay the penalty over and over again. If people don't have health insurance, that's on them. Don't penalize the people, fight for single payer instead, that will help Americans even more.

You mention the site in NY but notice if you look online many people aren't signing up for it, they're shocked at the prices lol.....don't make me pull out stats of enrollment......

I noticed you did nothing to explain what would occur if an emergency came up, you have no insurance, and your savings is looking like the only thing keeping you from bankruptcy. You also glossed over that worthless site that you so called researched that offers more expensive family insurance for your homegirl, but would deny real emergencies or have you pay far more out of pocket.

If an emergency comes up, I'll be fine don't worry about me. It's my responsibility, not yours or the bumbling failure known as Obama. Let me worry about it and others without insurance worry about it. FORCING people to buy into this wack ass law and be penalized for it is unacceptable, only 6 people enrolled in Obamacare the first day LOL, people aren't feeling the Unaffordable Care Act, despite your desperate attempts to make this law seem cool. If it's so cool why is it so ? expensive? Blame the insurance companies if you want, but Obama being a ? idiot, he's forcing us to sign up to these insurance companies LMAO!!!!!!!!!!!!!!!!!!

Forcing people to buy an expensive product that was written by large insurance companies looking to make extra millions is NOT GUCCI. 85% of Americans were satisfied with their health coverage before this terrible law took place, and those without insurance somehow made it out alright for the most part. The "worthless" site I mentioned may be just that, my research isn't done but again, I shouldn't be forced into anything. If Obama wants to make a law that says the uninsured will not get coverage for major surgeries if they can't afford it, then he should fight for that.

I predict this law will get even more unpopular as time goes on, and it absolutely will fail in a matter of time. The young and healthy aren't signing up for this ? , and the without us, the Unaffordable Care Act will collapse under its own weight as it can no longer afford itself. And meanwhile, Obama's approval ratings remain low, 41% according to Gallup.

You far too emotional my brother, we talking about all Americans, not just you, you selfish bastard. Don't you know that people without insurance end up in emergency rooms and raise cost? I would like to see a link for that 85% number.. What about the percentage of people that were unsatisfied after they actually had to use it for something serious? How about the percentage of people that were dropped for ? reasons? Gallup is wack and it was proven when they couldn't predict the presidential and congregational elections unlike Nate Silver. ? a poll, how about, it's the presidents duty to secure the safety of all Americans, and not create additional burdens on our healthcare system by having people handle their problems at the last minute and add less to the economy because of bankruptcy.. I guess you don't want social security either because we are forced to pay into that too.

How about you tell us more about your homegirl and the choices she has for affordable family care other then the ? link you posted.. -

LOL SMH Furiousone you still don't understand what UNAFFORDABLE means. You want me to get a dictionary for you? You want me to read one for you in a baby voice so you can understand? GOOGOO GAGA style? I can shake a baby toy for you as well as I type the definition.

You call me selfish but I'm not the one trying to force people onto expensive as hell insurance policies with crooked insurance companies. THAT IS SELFISH because Obama should be smart enough to know in this weak economy, MOST PEOPLE CAN'T AFFORD THESE PLANS. Only six people enrolled on the first day, out of 4.7 million people who shopped around LOL. Imagine if only 6 people bought Grand Theft Auto V its first day. Do you think most Americans are big balling Oprah or Michael Jordan style? It seems you do. The people without insurance can't afford it for the most part because the cost of living is too ridiculous here in America. It is the president's duty to help out Americans, not to further bankrupt their futures by making them pay into plans many just can't afford, while insurance companies try to make a killing. Social security we don't pay much into per paycheck, so that's not a good analogy.....

Before the Obamacare nightmare/epic disaster, most Americans polled were indeed happy with their healthcare. Here is a link showing what I mean.......

http://www.politifact.com/truth-o-meter/statements/2010/mar/10/george-will/will-says-95-percent-people-health-insurance-are-s/

Here's what we found, poll by poll, in reverse chronological order:

• Quinnipiac University, Sept. 2009. "How satisfied are you with your health insurance plan?" 54 percent very satisfied, 34 percent somewhat. Total: 88 percent satisfaction.

• Quinnipiac University, June 2009. "How satisfied are you with your health insurance plan?" 49 percent very satisfied, 36 somewhat satisfied. Total: 85 percent satisfaction.

• ABC News/Washington Post, June 2009. "For each specific item I name, please tell me whether you are very satisfied with it, somewhat satisfied, somewhat dissatisfied or very dissatisfied. ... Your health insurance coverage." 42 percent very satisfied, 39 percent somewhat satisfied. Total: 81 percent satisfaction.

• Mathew Greenwald & Associates for the Employee Benefit Research Institute, May 2009. "Overall, how satisfied are you with your current health insurance plan?" 21 percent extremely satisfied, 37 percent very satisfied, 30 percent somewhat satisfied. Total: 88 percent satisfaction.

----Of course, you keep ignoring yourself the fact many people will remain uninsured due to the UNaffordable Care Act. You may think most Americans are big balling Franklin Clinton Grand Theft Auto V style, but that's not the case. As far as my homegirl, I already told you the cheapest plan she saw for the UNaffordable Care Act, $312 a month with subsidies, a plan that has thousand dollar plus DEDUCTIBLES covering only 70% of cost, LOL.....what part of UNAFFORDABLE don't you and the ? known as Obama understand?

-

kingblaze84 wrote: »Ehhh it won't be until a significant amount of time passes that the real cost and effects of the law can be seen.

It's too soon, has it even been a month yet?

People have to save up for retirement NOW. At this very moment, this is not something most Americans can afford, especially those with kids. Train fares are going up, rent is going up and so are diapers and food. Is NOW really the time to raise even further the cost of living...? How much time should we give this law?

First of all there's no way to know what the real costs are because the plan hasn't been fully implanted yet it just started on Oct 15th dude. That was literally 16 days ago lol.

There are far too many variables to consider to be making such sweeping statements like the ones you are making here.

This thing won't be fully implemented for months and it will be years before it can be properly judged.

A lot of these people are only looking at premiums also, not looking at the back end which is what happens when people let politics and emotions dictate their decision making.

Whether one likes it or not isn't important, what is important is if it turns out to be beneficial which can't be known after 16 days.

-

kingblaze84 wrote: »Ehhh it won't be until a significant amount of time passes that the real cost and effects of the law can be seen.

It's too soon, has it even been a month yet?

People have to save up for retirement NOW. At this very moment, this is not something most Americans can afford, especially those with kids. Train fares are going up, rent is going up and so are diapers and food. Is NOW really the time to raise even further the cost of living...? How much time should we give this law?

First of all there's no way to know what the real costs are because the plan hasn't been fully implanted yet it just started on Oct 15th dude. That was literally 16 days ago lol.

There are far too many variables to consider to be making such sweeping statements like the ones you are making here.

This thing won't be fully implemented for months and it will be years before it can be properly judged.

A lot of these people are only looking at premiums also, not looking at the back end which is what happens when people let politics and emotions dictate their decision making.

Whether one likes it or not isn't important, what is important is if it turns out to be beneficial which can't be known after 16 days.

We don't know what the real costs will be?? So um, how come prices are already available online lol....are those phantom prices? Cuz if it is, then the law really should be delayed. People are seeing the ? prices now and have every right to judge them. Until the prices come down NOW, people will continue hating on this travesty of a law and the hatred will only grow. If you online to different forums, the talk is very ugly about the UNaffordable Care Act. Hopefully those prices come down, and not in years, ? THAT. -

kingblaze84 wrote: »kingblaze84 wrote: »Ehhh it won't be until a significant amount of time passes that the real cost and effects of the law can be seen.

It's too soon, has it even been a month yet?

People have to save up for retirement NOW. At this very moment, this is not something most Americans can afford, especially those with kids. Train fares are going up, rent is going up and so are diapers and food. Is NOW really the time to raise even further the cost of living...? How much time should we give this law?

First of all there's no way to know what the real costs are because the plan hasn't been fully implanted yet it just started on Oct 15th dude. That was literally 16 days ago lol.

There are far too many variables to consider to be making such sweeping statements like the ones you are making here.

This thing won't be fully implemented for months and it will be years before it can be properly judged.

A lot of these people are only looking at premiums also, not looking at the back end which is what happens when people let politics and emotions dictate their decision making.

Whether one likes it or not isn't important, what is important is if it turns out to be beneficial which can't be known after 16 days.

We don't know what the real costs will be?? So um, how come prices are already available online lol....are those phantom prices? Cuz if it is, then the law really should be delayed. People are seeing the ? prices now and have every right to judge them. Until the prices come down NOW, people will continue hating on this travesty of a law and the hatred will only grow. If you online to different forums, the talk is very ugly about the UNaffordable Care Act. Hopefully those prices come down, and not in years, ? THAT.

I suggest you put your critical thinking hat on bro. Again you have to do the research to know whether it's worth it..I.E "the real cost".

Higher premiums for better plans are a given also. However are these plans better? Ehhh it's too early to tell. The coverage may be better and that excuses the higher premiums but like I said there are too many variables to consider.

However delaying it doesn't fix anything.

-

kingblaze84 wrote: »LOL SMH Furiousone you still don't understand what UNAFFORDABLE means. You want me to get a dictionary for you? You want me to read one for you in a baby voice so you can understand? GOOGOO GAGA style? I can shake a baby toy for you as well as I type the definition.

You call me selfish but I'm not the one trying to force people onto expensive as hell insurance policies with crooked insurance companies. THAT IS SELFISH because Obama should be smart enough to know in this weak economy, MOST PEOPLE CAN'T AFFORD THESE PLANS. Only six people enrolled on the first day, out of 4.7 million people who shopped around LOL. Imagine if only 6 people bought Grand Theft Auto V its first day. Do you think most Americans are big balling Oprah or Michael Jordan style? It seems you do. The people without insurance can't afford it for the most part because the cost of living is too ridiculous here in America. It is the president's duty to help out Americans, not to further bankrupt their futures by making them pay into plans many just can't afford, while insurance companies try to make a killing. Social security we don't pay much into per paycheck, so that's not a good analogy.....

Before the Obamacare nightmare/epic disaster, most Americans polled were indeed happy with their healthcare. Here is a link showing what I mean.......

http://www.politifact.com/truth-o-meter/statements/2010/mar/10/george-will/will-says-95-percent-people-health-insurance-are-s/

Here's what we found, poll by poll, in reverse chronological order:

• Quinnipiac University, Sept. 2009. "How satisfied are you with your health insurance plan?" 54 percent very satisfied, 34 percent somewhat. Total: 88 percent satisfaction.

• Quinnipiac University, June 2009. "How satisfied are you with your health insurance plan?" 49 percent very satisfied, 36 somewhat satisfied. Total: 85 percent satisfaction.

• ABC News/Washington Post, June 2009. "For each specific item I name, please tell me whether you are very satisfied with it, somewhat satisfied, somewhat dissatisfied or very dissatisfied. ... Your health insurance coverage." 42 percent very satisfied, 39 percent somewhat satisfied. Total: 81 percent satisfaction.

• Mathew Greenwald & Associates for the Employee Benefit Research Institute, May 2009. "Overall, how satisfied are you with your current health insurance plan?" 21 percent extremely satisfied, 37 percent very satisfied, 30 percent somewhat satisfied. Total: 88 percent satisfaction.

----Of course, you keep ignoring yourself the fact many people will remain uninsured due to the UNaffordable Care Act. You may think most Americans are big balling Franklin Clinton Grand Theft Auto V style, but that's not the case. As far as my homegirl, I already told you the cheapest plan she saw for the UNaffordable Care Act, $312 a month with subsidies, a plan that has thousand dollar plus DEDUCTIBLES covering only 70% of cost, LOL.....what part of UNAFFORDABLE don't you and the ? known as Obama understand?

But you just told me you did research for a cheaper plan and your homegirl is playing 3 hunned but you then pointed me to a site that cost more for families (she has two kids) and it may not have a deductible, but it doesn't cover critical ? either. What it will do is leave you with a far larger medical bill. How is that affordable? Social security is still taking money out your pocket and many republicans believe the government shouldn't take anything which is unreasonable. How is only %70 bad when you barely got %0 for serious conditions after all you paid in beforehand. You keep glossing over all the negatives that existed before that the Affordable Care Act has rectified. I'm glad life isn't a videogame and we aren't measuring success by first week sales. You're baby language is appropriate for your attitude, now take a nap. Lmao at somewhat satisfied. What does that even mean? -

kingblaze84 wrote: »kingblaze84 wrote: »Ehhh it won't be until a significant amount of time passes that the real cost and effects of the law can be seen.

It's too soon, has it even been a month yet?

People have to save up for retirement NOW. At this very moment, this is not something most Americans can afford, especially those with kids. Train fares are going up, rent is going up and so are diapers and food. Is NOW really the time to raise even further the cost of living...? How much time should we give this law?

First of all there's no way to know what the real costs are because the plan hasn't been fully implanted yet it just started on Oct 15th dude. That was literally 16 days ago lol.

There are far too many variables to consider to be making such sweeping statements like the ones you are making here.

This thing won't be fully implemented for months and it will be years before it can be properly judged.

A lot of these people are only looking at premiums also, not looking at the back end which is what happens when people let politics and emotions dictate their decision making.

Whether one likes it or not isn't important, what is important is if it turns out to be beneficial which can't be known after 16 days.

We don't know what the real costs will be?? So um, how come prices are already available online lol....are those phantom prices? Cuz if it is, then the law really should be delayed. People are seeing the ? prices now and have every right to judge them. Until the prices come down NOW, people will continue hating on this travesty of a law and the hatred will only grow. If you online to different forums, the talk is very ugly about the UNaffordable Care Act. Hopefully those prices come down, and not in years, ? THAT.

I suggest you put your critical thinking hat on bro. Again you have to do the research to know whether it's worth it..I.E "the real cost".

Higher premiums for better plans are a given also. However are these plans better? Ehhh it's too early to tell. The coverage may be better and that excuses the higher premiums but like I said there are too many variables to consider.

However delaying it doesn't fix anything.

Delaying the law gives the law a chance to improve though doesn't it? Several Democrats are on record as saying this. As far as the sky high premiums for most people, should people just be happy with that?

You say whether people like it or not is not important but if the law is unpopular enough, too many people are gonna sit out and the law won't be able to afford itself, as the young and healthy will not contribute to it. They'll just opt for the penalty, and costs for the law will explode further. So therefore, it is important that people like the law. Prohibition didnt last cuz people kept drinking anyway. Slavery didn't last cuz there was too much uproar and bloodshed surrounding it.

OH and the UNaffordable Care Act started Oct 1.....it's been a full month. -

FuriousOne wrote: »kingblaze84 wrote: »LOL SMH Furiousone you still don't understand what UNAFFORDABLE means. You want me to get a dictionary for you? You want me to read one for you in a baby voice so you can understand? GOOGOO GAGA style? I can shake a baby toy for you as well as I type the definition.

You call me selfish but I'm not the one trying to force people onto expensive as hell insurance policies with crooked insurance companies. THAT IS SELFISH because Obama should be smart enough to know in this weak economy, MOST PEOPLE CAN'T AFFORD THESE PLANS. Only six people enrolled on the first day, out of 4.7 million people who shopped around LOL. Imagine if only 6 people bought Grand Theft Auto V its first day. Do you think most Americans are big balling Oprah or Michael Jordan style? It seems you do. The people without insurance can't afford it for the most part because the cost of living is too ridiculous here in America. It is the president's duty to help out Americans, not to further bankrupt their futures by making them pay into plans many just can't afford, while insurance companies try to make a killing. Social security we don't pay much into per paycheck, so that's not a good analogy.....

Before the Obamacare nightmare/epic disaster, most Americans polled were indeed happy with their healthcare. Here is a link showing what I mean.......

http://www.politifact.com/truth-o-meter/statements/2010/mar/10/george-will/will-says-95-percent-people-health-insurance-are-s/

Here's what we found, poll by poll, in reverse chronological order:

• Quinnipiac University, Sept. 2009. "How satisfied are you with your health insurance plan?" 54 percent very satisfied, 34 percent somewhat. Total: 88 percent satisfaction.

• Quinnipiac University, June 2009. "How satisfied are you with your health insurance plan?" 49 percent very satisfied, 36 somewhat satisfied. Total: 85 percent satisfaction.

• ABC News/Washington Post, June 2009. "For each specific item I name, please tell me whether you are very satisfied with it, somewhat satisfied, somewhat dissatisfied or very dissatisfied. ... Your health insurance coverage." 42 percent very satisfied, 39 percent somewhat satisfied. Total: 81 percent satisfaction.

• Mathew Greenwald & Associates for the Employee Benefit Research Institute, May 2009. "Overall, how satisfied are you with your current health insurance plan?" 21 percent extremely satisfied, 37 percent very satisfied, 30 percent somewhat satisfied. Total: 88 percent satisfaction.

----Of course, you keep ignoring yourself the fact many people will remain uninsured due to the UNaffordable Care Act. You may think most Americans are big balling Franklin Clinton Grand Theft Auto V style, but that's not the case. As far as my homegirl, I already told you the cheapest plan she saw for the UNaffordable Care Act, $312 a month with subsidies, a plan that has thousand dollar plus DEDUCTIBLES covering only 70% of cost, LOL.....what part of UNAFFORDABLE don't you and the ? known as Obama understand?

But you just told me you did research for a cheaper plan and your homegirl is playing 3 hunned but you then pointed me to a site that cost more for families (she has two kids) and it may not have a deductible, but it doesn't cover critical ? either. What it will do is leave you with a far larger medical bill. How is that affordable? Social security is still taking money out your pocket and many republicans believe the government shouldn't take anything which is unreasonable. How is only %70 bad when you barely got %0 for serious conditions after all you paid in beforehand. You keep glossing over all the negatives that existed before that the Affordable Care Act has rectified. I'm glad life isn't a videogame and we aren't measuring success by first week sales. You're baby language is appropriate for your attitude, now take a nap. Lmao at somewhat satisfied. What does that even mean?

AHAHAHA!!!! Obamacare has RECTIFIED problems with healthcare?? Are you ? kidding me? LOL WOWWWWW......premiums are up, costs are up, deductibles are up and worst of all, people who WERE happy with their healthcare plans are getting them cancelled in the mail by the millions. I never glossed over the negatives as to life before the UNaffordable Care Act, too many were uninsured true. But 85% of Americans on avg based on the polls I showed you stated that most Americans who DID have health insurance were satisfied because it met their basic needs, even if it wasn't ultra fancy. I just found out my boy got his healthcare plan cancelled today, and he was happy with it because it took care of him when he went through neck surgery. Now he's gonna be paying more in premiums and deductibles based on what he's seen on the website. He voted for Obama twice and now hates him more then Twatgetta does.

As far as the AMG website, remember I'm not finished doing my research on it and other private insurers.

The UNaffordable Care Act is a giant scam written by insurance companies, and the bronze and silver plans, according to research I'm doing, will NOT be accepted by various hospitals and doctors LOL....this is the law I'm supposed to be happy about?

If you're trying to get me to like Obamacare, you're frankly wasting your time. I know the prices that I have seen, and it SUCKS. NOTHING WILL CHANGE THAT unless the law is delayed and fixed, or destroyed completely.

-

smh @ Kingblaze just instantly co-signing every anti-obamacare horror story and narrative out there cuz he hate dude so much. Couple of website glitches and people paying higher prices and suddenly the Tea Party is 100% right. ? outta here. Obamacare already saved sick kids kids with cancer, already saved me from emergency surgery that woulda cost thousands. And you wanna call the ? a joke because YOU haven't benefitted yet, you ignorant self-centered muhfucka....

Since you apparently know jack ? about the complex, BADLY NEEDED Health Care Reform you're suddenly prescribing solutions and fixes and really bad ideas for (ask Paul Krugman about killing the mandate), and since you apparently want this to just be your lil stickied anti-obamacare thread, I'mma regularly drop ? knowledge on yo ass from Progressive blogs because all you apparently read is that Reason Magazine "libertarian" ? . Maybe you'll learn something before you start canvassing for Rand Paul....

President Obama’s claim that if an individual likes their health care coverage in 2009 or 2010 is technically true but misleading. It is true that if there has been no plan changes in benefits, network, tiering or basic eligibility, a plan that does not meet PPACA requirements for life time limits, coverage of essential health benefits and community underwriting can continue to go forth in the marketplace for as long as someone will buy it but the practical impact is that there are very few stable plan designs of more than a few years.

The grandfather regulations and definitions are at the link below. I’ll summarize before most of the readers here fall asleep.

http://www.balloon-juice.com/wp-content/uploads/2013/11/HHS-OS-2010-0015-0001.pdf

Plans are grandfathered past some Obamacare regulations for plans that had membership before PPACA was signed into law and the following items were not significantly changed:

Out of pocket limits, co-pays, deductibles and co-insurance levels

Covered services

Eligibility requirements for members

Employee contributions to premiums if group coverage, or total premium for individual coverage

Grandfather plans were destined to die rather quickly due to underlying trends in the insurance market. Over the past twenty years, deductibles have increased, co-insurance has increased, out of pocket maxes have increased, and employee contributions to the premiums have increased. This was trend and it would have continued even if the firebaggers were successful in killing the bill.

In year 1, most plans were grandfathered but some plans became PPACA compliant as deductibles increased, co-pays increased and employee contributions increased as employers sought to decrease the amount of increase that they paid in health benefits. In year 2, fewer plans were grandfathered as more benefit design and payment design changes occurred. Now, in year 3, there are still a few grandfathered plan designs available, but most plans and employer sponsored groups are using PPACA compliant designs.

It is quite possible for a plan to stay grandfathered for a decade. I will be shocked if my company has no grandfathered plans in 2020; we won’t have many, but we’ll have at least one or two groups clinging to their 2009 plan design.

So, it is true that if you liked your 2010 insurance plan AND there were no material changes to it, you can keep it. It is just extremely unlikely that there are no material changes to your plan.

http://www.balloon-juice.com/2013/11/01/where-grandfathers-go-to-die/

Most people are minimally impacted by Obamacare as they already get their insurance through an employer, through the government or have solid individual coverage. The next largest group of Americans are impacted by Obamacare as they’ll be gaining access to coverage. They’re better off. Then there are two small groups. The first is a group who has decent individual coverage but may or may not be better off with the improved coverage mandates of Obamacare. These situations will vary by individual income and thus subsidy status, state and health status. The other group are the clear losers of the policy changes. They have individual coverage that is being cancelled and Exchange coverage is more expensive.

So what types of plans are in the “Potential Loser” bucket?

Let’s go back to a post on Premium ? for a quick review:

Arkansas: $26 per month for a $25,000 deductible 23% applicants denied. 28% uprated.

Ohio: $25,000 deductible, 19% denied, 17% uprated.

Let’s look at a the Arkansas plan in some more detail, as we go to page four to see what is not covered. I’ll highlight some of the more unusual things that are not covered.

Maternity coverage on the base plan.

Maternity coverage or pre-natal care within the first twelve months of purchase of the maternity/pregnancy rider.

Any pre-exisiting condition for an adult within the first twelve months of purchase

A similar plan on the same information sheet has additional limitations. The HSA plan does not cover mental health treatments or prescriptions.

This is an extreme example. The Ohio plan in the link above is similar in that it excludes maternity care and pre-exisiting conditions but it does cover mental health needs.

Individuals with these types of plans, or basically any individual product that is medically underwritten, excludes maternity care and has a deductible over $10,000 is almost guaranteed to face sticker price rate shock as these plans don’t even come close to meeting minimal Obamacare standards of insurance. If the person facing sticker price rate shock for a basic Bronze or a Catastrophic plan is making under 250% of Federal Poverty Line, they’ll probably break about even as they move into an Exchange Bronze or Exchange Catastrophic plan. If they make more than 250% FPL, they most likely are getting much better coverage (that they individually probably don’t need as they demonstrated no history of medical need) at a significantly higher post-subsidy price. And for the individuals in this bucket who make more than 400% FPL, they are guaranteed to face rate shock.

"Gee you had ? insurance and now you are forced to have decent insurance and pay more. Sucks to be you."

http://www.balloon-juice.com/2013/11/01/whats-in-the-3/ -

@kingblaze84 , now you're just being fallacious? No positive changes? Word? I'm starting to think that you are making up these people so called unsatisfied people. Repeating your catch words often enough doesn't make it true.

-

Swiffness, you just dropped a big load of ? right now. You claim 80% of Americans won't be effected from the UNaffordable Care Act? So tell me what Obama officials meant by this in a 2010 memo..........

http://www.chicagotribune.com/features/chi-nsc-obama-officials-in-2010-93-million-americans-will-20131031,0,2636931.story

Obama Officials In 2010: 93 Million Americans Will Be Unable To Keep Their Health Plans Under Obamacare

Section 1251 of the Affordable Care Act contains what's called a "grandfather" provision that, in theory, allows people to keep their existing plans if they like them. But subsequent regulations from the Obama administration interpreted that provision so narrowly as to prevent most plans from gaining this protection.

"The Departments' mid-range estimate is that 66 percent of small employer plans and 45 percent of large employer plans will relinquish their grandfather status by the end of 2013," wrote the administration on page 34552. All in all, more than half of employer-sponsored plans will lose their "grandfather status" and get canceled. According to the Congressional Budget Office, 156 million Americans-more than half the population-was covered by employer-sponsored insurance in 2013.

Another 25 million people, according to the CBO, have "nongroup and other" forms of insurance; that is to say, they participate in the market for individually-purchased insurance. In this market, the administration projected that "40 to 67 percent" of individually-purchased plans would lose their Obamacare-sanctioned "grandfather status" and get canceled, solely due to the fact that there is a high turnover of participants and insurance arrangements in this market. (Plans purchased after March 23, 2010 do not benefit from the "grandfather" clause.) The real turnover rate would be higher, because plans can lose their grandfather status for a number of other reasons.

How many people are exposed to these problems? 60 percent of Americans have private-sector health insurance-precisely the number that Jay Carney dismissed. As to the number of people facing cancellations, 51 percent of the employer-based market plus 53.5 percent of the non-group market (the middle of the administration's range) amounts to 93 million Americans.

----So what the hell were you saying again????? -

Our guest today is Greta Frost, who says she's angry that President Obama took away her health care plan that she was very happy with. Greta, can you tell us what happened?

Thank you, Dana. Well, I work as a cashier at a diner and we were all getting along quite fine without a health plan until Darla, one of the waitresses, got a goiter and the hospital costs got so much she had to move to a shipping container over by the rail yard and now the only kind of bath she can get is in the sink in our Ladies' Room. So I went shopping for a group plan, but since so many of the workers at the diner are young and believe all that Obamacare nonsense they didn't want to go in on it, so I put together an application with some ladies here in Durham who like to get together and watch Modern Family every week.

We got a policy from a company called ClarioCare, which was a division of Shepard's Heating and Cooling, and while $310 a month sounds like a lot of money, it was much better than what the others were charging, and I found that it suited my needs. Naturally there were some things they couldn't cover, like my hysterectomy. And I understand that, they're a business, they have to make money same as we all do.

But they were there for me in other ways. For example, last year I cut my finger pretty bad on a slicer at work, and they shipped me next-day air a big box of Band-Aids, or I should say Curad strips. When I wrote back and told them that the Curad strips didn't stick very well to my skin, they wrote right back to apologize and explained that all their Curad strips had got soaked in Hurricane Sandy, and they sent another big box of Curad strips and a tub of Elmer's Glue-All. So I felt like they were really looking out for me.

Well, last week I got this letter from ClarioCare and I was fit to be tied because it said thanks to Obama, not only were they going to get rid of my policy, but they were getting out of the insurance business altogether to concentrate on heating and cooling and also real estate, and they sent me a free invitation to a seminar about that as a parting gift. I appreciated the gesture but what I did not appreciate was Obama taking away this insurance plan that I was very happy with. If I cut myself again, or, ? forbid, get cancer, who's going to send me Curad strips? So I haven't even been to that Obamacare website which I hear doesn't work anyway, and I'm not going to call them on the phone or send in any forms. Instead I'm going around to all the talk shows that the nice people from that Foundation want to put me on, and tell people my story, and I'm sure once they've heard it, they'll agree that the answer to all our health care problems in this country is health savings accounts and tort reform.

http://alicublog.blogspot.com/2013/11/vox-populi.html#disqus_thread

Damn that mean ol' Obamacare! Why did Obama have to do this!!! -

No. It's delaying the inevitable.kingblaze84 wrote: »kingblaze84 wrote: »kingblaze84 wrote: »Ehhh it won't be until a significant amount of time passes that the real cost and effects of the law can be seen.

It's too soon, has it even been a month yet?

People have to save up for retirement NOW. At this very moment, this is not something most Americans can afford, especially those with kids. Train fares are going up, rent is going up and so are diapers and food. Is NOW really the time to raise even further the cost of living...? How much time should we give this law?

First of all there's no way to know what the real costs are because the plan hasn't been fully implanted yet it just started on Oct 15th dude. That was literally 16 days ago lol.

There are far too many variables to consider to be making such sweeping statements like the ones you are making here.

This thing won't be fully implemented for months and it will be years before it can be properly judged.

A lot of these people are only looking at premiums also, not looking at the back end which is what happens when people let politics and emotions dictate their decision making.

Whether one likes it or not isn't important, what is important is if it turns out to be beneficial which can't be known after 16 days.

We don't know what the real costs will be?? So um, how come prices are already available online lol....are those phantom prices? Cuz if it is, then the law really should be delayed. People are seeing the ? prices now and have every right to judge them. Until the prices come down NOW, people will continue hating on this travesty of a law and the hatred will only grow. If you online to different forums, the talk is very ugly about the UNaffordable Care Act. Hopefully those prices come down, and not in years, ? THAT.

I suggest you put your critical thinking hat on bro. Again you have to do the research to know whether it's worth it..I.E "the real cost".

Higher premiums for better plans are a given also. However are these plans better? Ehhh it's too early to tell. The coverage may be better and that excuses the higher premiums but like I said there are too many variables to consider.

However delaying it doesn't fix anything.

Delaying the law gives the law a chance to improve though doesn't it? Several Democrats are on record as saying this. As far as the sky high premiums for most people, should people just be happy with that?

Like I said previously higher premiums = better coverage. If you can prove they aren't or won't be getting better coverage you would have a point.You say whether people like it or not is not important but if the law is unpopular enough, too many people are gonna sit out and the law won't be able to afford itself, as the young and healthy will not contribute to it. They'll just opt for the penalty, and costs for the law will explode further. So therefore, it is important that people like the law. Prohibition didnt last cuz people kept drinking anyway. Slavery didn't last cuz there was too much uproar and bloodshed surrounding it.

Most young and healthy people don't get insurance anyway that has nothing to so with ACA.

Being popular isn't the same as being beneficial, and if nobody buys it then so be it. ? will just be uninsured and paying fines, that's it. I don't care honestly...OH and UNaffordable Care Act started Oct 1.....it's been a full month.

One whole month? Wow that's a looooooong time. I mean wow, a whole month really? I guess we can say the law is fully implemented then? -

FuriousOne wrote: »@kingblaze84 , now you're just being fallacious? No positive changes? Word? I'm starting to think that you are making up these people so called unsatisfied people. Repeating your catch words often enough doesn't make it true.

I'm making up these so called unsatisfied people? Why don't you go to Obamacarehorrorstories.com and see even WORSE stories then the ones from people I know. You try telling people on that site how great the UNaffordable Care Act is.

Aight I gotta give this thread a break, I'm at work and will be going on a nice vacation soon.....I'll be back soon enough and I'm sure the horror stories will only get worse.........thankfully, I'm not alone in my feelings and strongly believe this law will either be destroyed or fixed up due to the overwhelming NEGATIVE feedback from this terrible law. -

kingblaze84 wrote: »FuriousOne wrote: »@kingblaze84 , now you're just being fallacious? No positive changes? Word? I'm starting to think that you are making up these people so called unsatisfied people. Repeating your catch words often enough doesn't make it true.

I'm making up these so called unsatisfied people? Why don't you go to Obamacarehorrorstories.com and see even WORSE stories then the ones from people I know. You try telling people on that site how great the UNaffordable Care Act is.

Aight I gotta give this thread a break, I'm at work and will be going on a nice vacation soon.....I'll be back soon enough and I'm sure the horror stories will only get worse.........thankfully, I'm not alone in my feelings and strongly believe this law will either be destroyed or fixed up due to the overwhelming NEGATIVE feedback from this terrible law.

So i'm gonna go to a site that is dedicated to focusing on only bad things and you are saying you aren't inventing these friends of yours? At least i know where you are getting these stories of your so called friends from.. It seems you don't want ACA to work because you are a bit too focused on the tings that the republicans and tea party are creating to make sure it doesn't work or convince people that it doesn't. I mean, how else can you say with a straight face, that the ACA has no positive benefits? Be careful on your vacation without insurance, you're gonna drive up cost if you almost drown at the beach and they bring you to the ER. -

I can't wait to watch ? try to counter the info my posts with Thomas Sowell columns.....

"Despite a very rocky first month for the health insurance exchanges, public opinion on the health-care law did what it has done for the past three years: stayed exactly the same."

The gold standard of health care polling, the Kaiser Health Tracking Poll, is out for October and shows once again that the public is basically behind Obamacare, with significantly more wanting to keep it or expand it than to repeal it. Despite all of the Republicans' efforts to sabotage it, public opinion about Obamacare has held steady, 44 percent unfavorable versus 38 percent favorable, but large majorities are still opposed to Republican sabotage.

See my child, this has always been the trend. People fault Obamacare for not doing more. They want Single Payer, and they'll GET IT once the individual states like Cali start building Single Payer systems, thanks in part to................wait for it................the Affordable Care Act.

-

Obamacare is more than a website. More than half of the people I worked with on the Obama campaign in 2008 said health care reform was their reason for joining the campaign and working to elect a Democrat. Forty-seven million Americans, including me, were uninsured until now. When I finally was able to log into the site–after a few days and a few false starts–I was floored by the number of affordable options. When I scrolled through my list of choices–124 different plans to be exact–I realized that this is the reason Republicans hate the program so much: it will fundamentally change lives, including my own.

(but she's not kingblaze ergo its broken and obamas totally a sinking ship bro)

There are a few glaring omissions in the coverage of Obamacare’s shaky rollout. For the most part, those covering the problems are insured themselves and consequently greatly underestimate the patience of a chronically uninsured person who has been counting down the days until Obamacare began so they could have a little peace of mind that if they got sick they wouldn’t be staring down bankruptcy.

And while some young men may think they are invincible and don’t need health insurance, preventative care is not something that the majority of women can roll the dice with. Between recommended regular pap smears and appointments to access birth control, seeing a doctor is often a necessity. And, let’s be clear, thanks to Obamacare, young people can stay on their parents insurance until they are 26; By 27 young people, regardless of their gender, tend to be more responsible and much more risk averse.

The website problems are being fixed–the New York exchange that I am using to compare plans is working just fine as of this morning–and the Obama administration has promised to work on the glitches to ensure that Americans who will likely wait until the last minute to sign up will have a working website. Enrollment lasts until February 15th and the coverage begins January 1st. While the early website issues are frustrating, they by no means indicate that the program as a whole has failed.

And unless you are a journalist who has been chronically uninsured, your feigned frustration about website issues reeks of privilege. To me, a few website glitches are a lot less frustrating than having to use the same inhaler for over a year because I can’t afford to go the doctor. Perspective is everything.

http://feministing.com/2013/10/24/dear-journalists-your-privilege-is-clouding-your-perspective-on-obamacare-website-glitches/

no destroy obamacare it doesnt work -

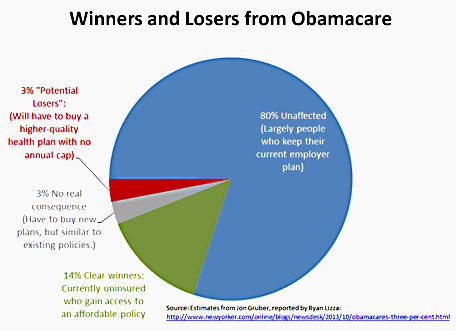

While President Obama was in Boston on Wednesday to deliver a speech at Faneuil Hall, he was also scheduled to attend a private meeting with friends and supporters. One of the well-wishers in attendance was Jonathan Gruber, an M.I.T. economist and an architect of both Mitt Romney’s health-care plan in Massachusetts and Obama’s Affordable Care Act…

Gruber’s view is that, at the moment, the technical problems associated with healthcare.gov are only a “DefCon 4 problem”—mostly just a political headache for the White House. (Five is the lowest level of alarm on the U.S. military’s defense-readiness-condition scale; one is the highest.)

http://www.newyorker.com/online/blogs/newsdesk/2013/10/obamacares-three-per-cent.html

My wife had cancer in 1994. The small business where she worked at the time lost their insurance over it. She hasn’t been insured for 19 years. The only bright spot: the indications that your leukemia is back include full-body bruising and blood coming out your ears when you floss. At least we haven’t spent the decades wondering if something was lurking that regular followups might have found.

In January 2005 her mammogram showed a mass. We knew that we were going to lose everything, as the best-case outcome. My wife went outside after listening to the voicemail (left at 4:55pm on a Friday asking her to come back in Monday morning but not saying why…) and smoked her last cigarette.

By Monday we’d found the baseline film, by Wed. the radiologist that Planned Parenthood referred her to (paid by the YWCA program for uninsured women) had matched them up. The lump was scar tissue from a bee sting in childhood. She still hasn’t smoked again, but that was the longest weekend of my life.

This is what it means to be uninsured: the news that your 5 year old may lose a parent in elementary school takes a backseat to ‘we’re going to lose the house…unless my wife dies quickly’.

I have melanoma, the cancer that lurks. I’m now on a followup schedule that continues until I die of something else, or the lurking semi-solid cells that are statistically likely to be somewhere in my body hit a switch and start to multiply again.

Our business has never been big enough to offer insurance. We knew from 1994 that plans to cover fewer than 50 people wouldn’t pay out or would take the premiums and run if we ever made a claim, so we didn’t bother to offer the option to make Blue Cross richer in order to feel insured. Obviously this has affected recruiting at our company.

Two critical points:

-In the past 4 weeks, I have received 5 resumes from exactly the kind of people we would like to hire more of. All say they’ll be available around the 1st of the year. Demographically they’re very different from the resumes I’ve seen over 15 years in this business. They’re younger and looking for fewer hours doing something they already know is hard in ways they enjoy. They can afford to leave Big Ugly Death Star Corp. because they can buy health insurance.

-I was diagnosed in Sept. 2011. Because my state had already implemented the part of the ACA that requires insurance companies to continue policies at similar rates EVEN IF the individuals on them make claims–not something we expected, after our earlier experience–I’m still insured.

(KINGBLAZE READ THAT AGAIN AND TELL ME AGAIN HOW OBAMACARE IS TERRIBLE BECAUSE IT HASN'T HELPED *YOU* YET, YOU SELFISH ? )

We’re going to buy an exchange plan that puts our family on one deductible and OOP max, for the first time ever, next week.

The technical issue we discovered with the web site was after applying: whoever coded the ‘citizenship for adopted people’ section of the eligibility database chose the wrong field type for the only way our government has to verify my kid lives here legally. So we have to talk to a manager with superpowers before we can choose among the 57 (!) options to get our family covered.

We can afford any of these plans. Fifty-seven choices. Sure, some of them aren’t appropriate for our family’s health profile (rare cancer=must have some out of network coverage; hearing aids for kid must be covered, etc.). Some of them cost more than I’d prefer to spend, once we add up the premium and deductible–which we anticipate meeting sometime in Feb. 2014, with the backlog of preventive and screening that Mrs Phoenix hasn’t had access to since before PET scans were invented.

But we get to buy insurance, in a market that has to take our money and has to pay for the health care we may need.

As a parent, a spouse and a small business owner, I would carry the Congresscritters and President who got us these solutions across a river of acid on my back to keep them.

http://thirdtimecharmed.com/wp/

Commenter "Phoenix Rising" -

I get it. The website for 40 million previously uninsured people who are now, because of the ACA, going to get healthcare coverage, sucked.

I just watched the SNL opening skit mocking Sebelius and ACA, and the only thing I could think was thank ? ALLAH that Social Security and Medicaid were rolled out in the pre-internet days.

Think about it, you ? ? at the Wonkblog and you other alleged liberals. All the programs you claim to love, like SS, Medicare, Medicaid, etc. At this point in the rollout for these programs 50, 60, and 70 years ago, the mail would just be reaching the respective offices. Problems people are experiencing today would not even be noticed for four months in those days, yet people still participated, just as people are right now.

…[T]he overwhelming majority of American businesses—ninety-six per cent—have fewer than fifty employees. The employer mandate doesn’t touch them. And more than ninety per cent of the companies above that threshold already offer health insurance. Only three per cent are in the zone (between forty and seventy-five employees) where the threshold will be an issue. Even if these firms get more cautious about hiring—and there’s little evidence that they will—the impact on the economy would be small.

Meanwhile, the likely benefits of Obamacare for small businesses are enormous. To begin with, it’ll make it easier for people to start their own companies—which has always been a risky proposition in the U.S., because you couldn’t be sure of finding affordable health insurance. As John Arensmeyer, who heads the advocacy group Small Business Majority, and is himself a former small-business owner, told me, “In the U.S., we pride ourselves on our entrepreneurial spirit, but we’ve had this bizarre disincentive in the system that’s kept people from starting new businesses.” Purely for the sake of health insurance, people stay in jobs they aren’t suited to—a phenomenon that economists call “job lock.” “With the new law, job lock goes away,” Arensmeyer said. “Anyone who wants to start a business can do so independent of the health-care costs.” Studies show that people who are freed from job lock (for instance, when they start qualifying for Medicare) are more likely to undertake something entrepreneurial, and one recent study projects that Obamacare could enable 1.5 million people to become self-employed.

Even more important, Obamacare will help small businesses with health-care costs, which have long been a source of anxiety… Small businesses often face so-called “experience rating”: a business with a lot of women or older workers faces high premiums, and even a single employee who runs up medical costs can be a disaster… Insurance costs small companies as much as eighteen per cent more than it does large companies; worse, it’s also a crapshoot. Arensmeyer said, “Companies live in fear that if one or two employees get sick their whole cost structure will radically change.” No wonder that fewer than half the companies with under fifty employees insure their employees, and that half of uninsured workers work for small businesses or are self-employed. In fact, a full quarter of small-business owners are uninsured, too…

The U.S. likes to think of itself as friendly to small businesses. But, as a 2009 study by the economists John Schmitt and Nathan Lane documented, our small-business sector is among the smallest in the developed world, and has one of the lowest rates of self-employment. One reason is that we’ve never had anything like national health insurance. In a saner world, changing this would be a reform that the “party of small business” would celebrate.

http://www.newyorker.com/talk/financial/2013/10/14/131014ta_talk_surowiecki -

I am SURE my story is not unique, but It SHOULD serve as a reality check for anyone who has been prone to believe any of the bushwah being peddled by the GOP/T, especially during the last two "Glitch-Hunts", I mean "hearings", led by Republicans who are STILL looking fo unfund a LAW duly passed and already in force.

As a self-employed person, I have RARELY enjoyed health care coverage from a group large enough to negotiate favorable coverage on my behalf. In the last few years I was insured, I was in the individual marketplace, which Secretary Sebelius properly characterized as "The Wild West" - and believe me, it WAS (and would STILL be if not for the ACA).

When I first entered the wild and wooly "Land of the Individual Policy", my first policy cost about $349 per month, with what I thought were reasonable compromises for deductibles and coverage limits.

As the years passed on, I noticed an alarming trend for my renewal premiums to head up like a rocket each renewal, while the services included started to plummet earthwards like a stone. from what I am reading in comments by others, this was apparently NORMAL for the individual plans.

During my time being insured, I used my benefits rarely, and mostly for the occasional test needed during a checkup visit, and don't recall EVER using MAJOR benefits.

But at my next renewal, I was unceremoniously offered a NEW premium, $800 PER MONTH, with a ridiculous annual deductible of about $10,000, and some other limits I honestly cannot remember at this time. But the policy wasn't great

I could not afford $800/mo, so I quietly dropped my coverage, having NO choice but to "run the risk" of going without, as many do when faced with similar unaffordable premiums.

A few years later, when the beginning symptoms of old-age diseases started to surface, I got scared and immediately contacted my insurer again to re-up, only to be told that I had been "red-lined" because I had dropped my previous coverage. And, oh , now we KNOW you have a pre-existing condition - so, sorry, NO insurance for YOU!

This took place in 2008 - I have been living in deathly fear of a major medical catastrophe ever since, and in 2011, it happened.

Alarming symptoms began to creep up on me, and got so bad that I when I talked to my primary care physician (who I could no longer afford to see often enough to have caught this early) he basically said: "You have congestive heart failure, and it will ? you - you have ONE choice - without insurance, you HAVE to head for the ER at the County Health Service, and GO NOW".

I did - and bless 'em, they admitted me within 15 minutes, being well aware of the gravity of my medical condition, and the serious nature of any delay. I spent a week in-hospital, admitted for the dangerous cardiac condition, and also because of a urological condition that complicated the course of treatment for the cardiac condition - the double whammy.

During that week, I encountered the BEST and WORST of health care practitioners - wonderful nurses and doctors who truly cared, and lackluster/hostile nurses in the surgical recovery unit where I spent the TWO WORST DAYS AND NIGHTS I have EVER experienced. But they saved my life.

I didn't WANT to rely on the County for medical care, but I had no choice - I just couldn't afford insurance - and I was damned glad the County health service was there!

It took a YEAR to get healed from both of my conditions, but as a bonus, the surgery that was undertaken to fix my urological condition nearly killed me when it led to uncontrolled internal bleeding.

I was taken to a local for-profit hospital against my will by the local EMS, who said they could NOT take me to the county health service where I already had coverage!. It took ANOTHER serious surgical procedure to repair the surgery botched by the County health service.

When it was all done, I got a bill for $85K for the original County services, and another bill for $60K from the local hospital (for a 4-day admission)

So here's my take on the ACA controvery, from someone who is still too young for Medicare, still currently uninsured, and definitely getting on in years:

I WANT Obamacare

I am one of MILLIONS who NEED Obamacare

I an THRILLED that I may FINALLY be able to obtain insurance again without having to deal with any of the issues that have excluded me from coverage since 2008!

But Republicans want to ? the ACA before I can get insurance!

So to all the Republicans who have been working hard to ? the ACA, or REPEAL/UNFUND it, now that millions of us are FINALLY SO close to obtaining the health insurance we have DESPERATELY WANTED and needed, I say the following:

SHAME ON YOU HEARTLESS ? !

Many of you profess to be "Christians", but YOUR glee and zeal in trying to repeal/de-fund the ACA is a most UN-Christian like behavior.

Yammering endlessly about how the flawed website launch proves the underlying law isn't workable is just so much BULL.

When Medicare Part D launched, it was screwed up too but Democrats worked WITH REPUBLICANS TO MAKE IT WORK FOR THE COUNTRY!

When Romneycare launched in Mass, it took TWO YEARS to get all the website issues worked out - but Romneycare was NEVER called an unworkable failure.

As for the ACA itself, you all in the GOP/T need to SHUT UP and GET OVER IT - the ACA is law of the land, and you haven't been able to ? it. You need to remember that you work for We, The People - NOT just your wealthy campaign contributors - you work for ALL of us! The MILLIONS of uninsured folks like ME, who NEED the ACA.

http://www.dailykos.com/story/2013/10/31/1251927/-The-ACA-GOP-Nightmare-godsend-for-ME

no the tea party is 100% right destroy obamacare -

knowledge, educating you savages....

In the latest scare tactic used and repeated over the last week is that doctors are going to refuse to accept Health Insurance Exchange policies. Reince Preibus said that to Chris Jansing Friday morning and she was clueless on how to challenge this bogus argument, but not others. This idea that doctors won't accept these policies is a talking point parroted by Congressional members hell bent upon derailing ACA. It's an old saw and it's wonkish to parse out the argument. That said, "Doctor's refusing to accept ACA Exchange policies" is a threat summed up in one word, hogwash.

That ship already sailed. Health insurers had to fulfill a requirement within the ACA that each policy had an "adequate provider network". So, this argument that doctors won't accept ACA policies is one year out of date. The physicians, hospitals, diagnostic centers and more have already seen the reimbursement fee schedules and signed up to take these insurance policies.

This isn't a new rule (pdf), it was published in the Federal Register 2012. NCQA the "deemed authority" agreed to change their accreditation standards. If health insurers wanted their policy to be accepted by the NCQA, and be accepted on the Health Insurance Exchange they have to comply with the "adequate network standards" (which is written in English, here (pdf)).

It's a statement full of buffalo feathers that I've detailed out below, however, if you want to skip to the story's end? Priebus is spouting balogna.

Reimbursements

After working in health care for a long time, you get used to hearing health care providers complain about low reimbursements. That's what we call it, "reimbursements". Those are the monies the doctor or hospital receives after successfully sending in an insurance claim on your behalf. We've heard doctors are refusing to take new Medicare patients, refusing Medicaid patients and now they are going to refuse to take ACA exchange policies. Will some doctors refuse to take ACA policies? It's a firm, "It depends".

Physicians have always been able to decide what insurance companies they will accept and which ones they won't and these decisions are based upon the insurer's fee schedule. Doctors are also allowed to say if they will or won't accept new patients under a specific plan. The reality is that there will always be a curmudgeonly provider who won't take a policy that another physician is willing if not eager to accept. If you live in a urban area there will be a good selection of doctors. In rural areas maybe not, but that's not new either. HPSAs (Health Provider Shortage Areas) are a problem under Medicare and physicians in that area receive extra funds for Medicare patients. Private insurers have similar programs. Will physicians drop out of the provider networks for ACA Exchange Policies? Only when their contract with the Insurer allows it and then, another provider is highly likely to take their place.

Health Exchange Policies Aren't Readily Identifiable

Health insurance policies issued via the exchanges won't have a "Scarlet Letter" branding them as an Exchange policy. It will be more subtle than that. They are individual policies that won't have a Group Number on them, but that's it. As I wrote earlier this week about 15 million people have individual health care policies. They are small business owners including accountants, lawyers, doctors, architects and independent insurance agents. It also includes small retailers, electricians, plumbers and anyone else who doesn't have employer provided insurance. A physician who says they will not accept Health Exchange policies will be likely to turn away good paying patients. That's not something any decent healthcare administrator would advise their client physicians to do. The only way a physician would know if the insurance policy is an "Exchange Policy" is if the patient says it is. The anti-discrimination aspects of the ACA further complicates this position.

Civil Rights

Some healthcare administrators are unsure how the Civil Rights Section 1557 of the ACA is going to play out or how it will impact decisions surrounding what insurances to accept. How the health exchange policies will work out is yet to be seen. The only remedy open to physicians is to opt out in toto and that's what the physicians who declined to sign contracts the Health Exchange Insurer Networks did.....months ago. However, if the doctor has a contract with United Health Care that renews in 2015 and United has exchange policies; the physicians won't be able to opt out of those patients. As a practical matter, the doctor won't be able to reliably segment out Health Exchange patients.

Section 1557 is the civil rights provision of the Affordable Care Act. Section 1557 prohibits discrimination on the ground of race, color, national origin, sex, age, or disability under “any health program or activity, any part of which is receiving Federal financial assistance … or under any program or activity that is administered by an Executive agency or any entity established under [Title I of ACA]….” Section 1557 is the first Federal civil rights law to prohibit sex discrimination in health care. To ensure equal access to health care, Section 1557 also applies civil rights protections to the newly created Health Insurance Marketplaces established under the Affordable Care Act.

Section 1557 is consistent with and promotes several of the Administration’s key initiatives that advance prevention and wellness, reduce health disparities, and improve access to health care services. The Office for Civil Rights in HHS is responsible for enforcing Section 1557 with respect to covered programs. The law was effective upon enactment and OCR has been accepting and investigating complaints under this authority. If you believe you have been discriminated against on one of the bases protected by Section 1557, you may file a complaint with OCR. OCR also addresses Section 1557 in conducting outreach and providing technical assistance to covered entities and consumers.

Any provider or health plan that is receiving payments under a government program has to comply with this directive. This includes any physician receiving payments for medical studies, pharmaceutical studies, federal grants or those who accept Medicare, Medicaid, Tricare, SCHIP, FECA Black Lung patients. It also applies to health insurers who receive the subsidies people receive on the Health Insurance Exchanges who will have to enforce this measure in their provider contracts. If past experience with HIPAA is any indicator, the Office of Civil Rights will issue directives for Corrective Action for a few years before they impose sanctions for violations. Until then, look for people to error on the side of prudence.

Bottom Line

The Health Insurance Exchange policies already have their doctor and hospital networks set up. The contracts are signed. They are ready to go. If you want to know if your doctor is on the list, call them and ask. Meanwhile, my original assessment stands. That's hogwash.

http://www.dailykos.com/story/2013/11/01/1252301/-Another-ACA-Empty-Threat -

FuriousOne wrote: »So i'm gonna go to a site that is dedicated to focusing on only bad things and you are saying you aren't inventing these friends of yours? At least i know where you are getting these stories of your so called friends from.. It seems you don't want ACA to work because you are a bit too focused on the tings that the republicans and tea party are creating to make sure it doesn't work or convince people that it doesn't. I mean, how else can you say with a straight face, that the ACA has no positive benefits? Be careful on your vacation without insurance, you're gonna drive up cost if you almost drown at the beach and they bring you to the ER.

Quoted for ? emphasis. Kingblaze is at the point where he'd stop breathing if Obama was pro-oxygen LOL.kingblaze84 wrote: »----So what the hell were you saying again?????

You didn't even read what I posted about Grandfathered plans, did you? LOL you about as literate as your Tea Party friends. TL;DR the ACA forced all the Insurance Companies to upgrade their old plans, so the ? you want the old ? plan for, b? Its okay - I'll wait for you to browse some Right Wing propaganda sites and corporate media hit pieces for a rebuttal.

Lest we forget, Kingblaze wanted Obama to commit political suicide and cave to the Teahadists insane demands on the first page of this thread. He doesn't understand policy as well as he likes to think he does. His heart is in the right place, but he is a smartdumb ? when it comes to this political wonk ? . He needs things explained to him. I understand....the complexities can be difficult to grasp. There's a lot of numbers and stuff.

The Affordable Care Act requires health insurance issuers to submit data on the proportion of premium revenues spent on clinical services and quality improvement, also known as the Medical Loss Ratio (MLR). It also requires them to issue rebates to enrollees if this percentage does not meet minimum standards. MLR requires insurance companies to spend at least 80% or 85% of premium dollars on medical care, with the review provisions imposing tighter limits on health insurance rate increases. If they fail to meet these standards, the insurance companies will be required to provide a rebate to their customers starting in 2012.

Basically it goes as follows:

Because of state regulatory issues, insurance companies have an incentive to overprice their policies, because they are serving a new (broader) market, and because the state rate setting bureaucracy is slow and cumbersome.

If this is true, then the 80% medical loss ratio requirements will mean that they have to issue refunds to people at the end of the year.

So, this means that it is pretty likely that a lot of people will be getting refunds in early 2015.

Looking at this through my political lens, it looks pretty good.

http://www.dailykos.com/story/2013/10/31/1252145/-OK-This-is-a-Masterstroke-by-Obama

HAHAHAHAHAHAHA just admit you don't know much of ? about The Affordable Care Act, dude.

I will BET MONEY that Kingblaze never heard of the Medical Loss Ratio until this post. SMH...........

How can you say a law needs "MAJOR CHANGES" when you literally know nothing about it past a few bad news stories and your own limited experience with it? -

I know reading boring informative stuff isn't as fun as playing Madden and watching porn, but just hear me out...!

The health-care debate has suddenly come to focus almost obsessively on the alleged victims of Obamacare, who have lost their cheap individual insurance.

The idea underlying this notion, while facially appealing, is in fact misguided and morally perverse. No decent health-care reform can keep in place every currently existing private plan.

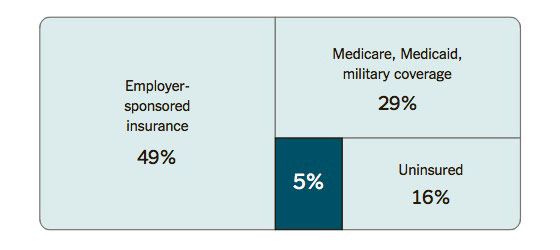

The New York Times has a helpful graphic displaying the structure of the insurance market:

The left and top-right squares show the four fifths of Americans who get coverage through the government. Those on the left who get covered through their employer get tax-subsidized insurance, and those in the top right get insured by the government directly. Obamacare leaves that structure in place (though it has a series of mechanisms designed to hold down their cost inflation).

The main coverage provisions affect the people in the bottom right quadrant. Most of that quadrant lacks any insurance at all, which points to the dysfunctionality of buying individual insurance before Obamacare. Some of them — 5 percent of the population — have a health-insurance plan. Health-care reforms have always thought of the people within that segment as being essentially the same group of people. Those are mainly healthy, non-poor people who have been skimmed out of the insurance pool, leaving behind those too poor, or too likely to need medical care.

Obamacare is designed to pool the bottom-right quadrant into risk pools, somewhat like the people on the left and the upper right. The poorest of the uninsured are eligible for Medicaid, though a Republican Supreme Court and Republican state governments collectively decided to leave them uninsured. The rest have coverage through the new health exchanges. By design, those exchanges prevent insurers from skimming out the healthy and excluding the sick. Some of the 5 percenters will get less expensive health care, mainly because they qualify for tax credits. Others think they will have to pay higher costs but, upon inspection, will be getting cheaper coverage on the exchanges.

But some other portion — an as-yet-undefined fraction of the 5 percent — will actually be paying higher insurance premiums in the exchanges, and their complaints are echoing across the land. Should we feel concerned for their plight? No, we should not, for three reasons.

First, a great many of the people who are happy with their individual health-insurance plan are happy only because they are unaware of its actual value. This sounds patronizing, but it also happens to be demonstrably true. Even highly educated consumers within this market were frequently snookered by insurance plans that turned out to leave them exposed to surprise costs — they incur a sudden high medical cost and discover their plan does not actually cover them. The fine print is a game of wits between insurer and customer that the insurer always wins. A large share of the people telling us now they’re happy with their individual insurance simply haven’t been exposed to a negative surprise. The handful of reporters who closely followed the individual-insurance market before last week are all watching the eulogies for the lost individual plans and having their brains explode.

Second, it is true that some people actually are getting decent individual health insurance, and have to pay more under Obamacare. Before, insurers could charge them a rate based on their individual likelihood of needing medical care, and some people are lucky enough to present a very low actuarial health risk. Now those people will have to pay a rate averaging in the cost of others who are less medically fortunate.

Have those healthy 5 percenters who do have decent insurance “lost” under Obamacare? In the very immediate sense, yes. That is what Obamacare advocate Jon Gruber is getting at when he concedes that 3 percent of Americans will be worse off under the new law. They’ll be paying higher rates in 2014 than they would have.

Yet this takes an oddly narrow view of their self-interest. You may pose a low actuarial risk today, but you cannot be certain your luck will continue for the rest of your life (or until you qualify for Medicare). Even people living the healthiest lifestyles suffer illnesses and accidents, or marry people who have a ? . Those who are paying a higher rate are getting something for their money: a guarantee that some future misfortune won’t lock them out of the market. You might call such a guarantee “insurance.”

So some of the 5 percenters are wrong, some of them are short-sighted, but they have identified a basic moral principle: Why is it fair to steal from them, the healthy, and give to others, who are sick? If they have truly mastered the fine print of the individual insurance market and want to gamble on remaining a good actuarial risk forever, should they be permitted to keep their winnings? Having drilled down through the practical arguments, here we get to the final reason, the moral bedrock of the issue.

Their objection has an intuitive, libertarian appeal that obscures the fact that the vast majority of insured Americans already submit to this form of redistribution. Indeed, they’re submitting to a much more stringent form of this redistribution. The exchanges are allowed to charge older people up to three times the premium they charge the young. But in the employer system, they’re not allowed to charge older people any higher rate at all. The shift from healthy to sick in the employer insurance pool is massive. Adrianna McIntyre, a 24-year-old wonk prodigy, notes that her employer-based coverage charges her more than three times the rate she could get in the new exchanges.